Active vs Passive Mutual Funds: Which Strategy Maximizes Returns? This question sits at the center of every investor’s decision-making process. Whether you’re building long-term wealth or optimising short-term gains, understanding how these two strategies differ can shape your financial future. Active funds rely on fund managers to outperform the market, while passive funds simply track an index at a lower cost. For investors trying to choose the better path, analysing returns, risk levels, cost impact, and performance consistency becomes essential. This introduction sets the stage to explore which strategy can truly maximise your returns.

What Are Active and Passive Mutual Funds? Key Differences Explained

Active mutual funds are managed by fund managers who make decisions about stock selection, sector allocation, timing and more, with the aim of outperforming a benchmark index. On the other hand, passive mutual funds (or index funds) simply aim to replicate a benchmark index (for example, the Nifty 50 in India) by holding the same stocks in roughly the same proportions, without trying to beat it.

The key differences for investors are:

- Strategy: Active = “beat the market”; Passive = “match the market”.

- Management involvement: Active = frequent decisions, more trading; Passive = minimal trading, mostly buy-and-hold.

- Cost: Active funds incur higher expense ratios because more research, trading and management are involved; passive funds have lower costs.

- Risk & flexibility: Active funds have more flexibility, but also more risk (manager risk, timing risk); passive funds have less flexibility but fewer layers of “human error”.

For an investor wondering “which strategy maximizes returns?”, understanding these differences is the first step.

How Active Fund Managers Aim to Beat the Market: Strategies and Techniques

For investors willing to choose active funds, the hope is that the fund manager’s skills and decisions add value. Active managers might:

- Identify undervalued stocks or sectors ahead of the market.

- Tilt the portfolio toward themes or opportunities that they believe will outperform (for example, small-cap companies, turnaround stories, etc.).

- Adjust sector weights dynamically (e.g., increasing exposure to a sector if they expect growth, reducing exposure if they expect risk).

- Employ tactical trading: changing holdings quickly to exploit market inefficiencies or shifts.

However, the challenge is that in many markets, especially large-cap and highly efficient markets, there’s limited room for outperforming. As one analysis of India showed: many large-cap active funds had an “active share” (portion of portfolio different from the benchmark) of around ~40%. That means ~60% of their portfolio mimics the index anyway, making it difficult to outperform.

Also, to beat the index by just a little, the active fund manager must generate excess return on that 40% sufficiently after paying higher costs.

For you as an investor, if you believe in the manager’s ability, have the patience and accept the higher cost and risk, active funds may make sense — but it’s not guaranteed.

Why Passive Mutual Funds Often Outperform in the Long Run:

From the investor’s perspective, passive funds carry a strong appeal: lower cost, transparency, simplicity, and historically respectable performance. Some of the key reasons:

- Lower fees mean less drag on returns. For example, in India the regulatory upper limit on expense ratio for equity funds has been set (e.g., first ₹500 crore AUM: 2.25%, next ₹250 crore: 2.00%, etc) which impacts active funds more than passive ones.

- The majority of actively managed funds have difficulty consistently outperforming the benchmark. A recent industry study found that over the 10-year period up to 2024 in the US, less than 22 % of active large-cap funds survived to beat their index peers.

- In India, the S&P Dow Jones SPIVA India scorecard shows that in the large-cap category a majority (~66%) of actively managed funds failed to beat their benchmark.

- Because passive funds simply track the index, they eliminate manager risk (i.e., risk of a bad manager), reduce trading costs and turnovers, and deliver market returns — which for many investors, over time, is very acceptable.

For you, as an investor focusing on returns, passive funds represent the “market return at low cost” option — and in many cases they perform better on a risk-adjusted basis than actively managed funds with higher costs.

Risk Comparison: Which Strategy Exposes Your Portfolio to Higher Volatility?

Risk and return go hand-in-hand. When choosing between active vs passive mutual funds, you need to examine not just potential returns but also risk exposure.

- Active funds typically have higher volatility because of more frequent trading, sector/stock bets, and reliance on manager decisions. For investors this means more uncertainty.

- Passive funds, since they mirror a broad-based index, usually have lower relative volatility (though they still carry market risk).

- Studies in India show that active funds often had higher standard deviation (SD) and higher beta compared to their passive counterparts. For example one paper found active funds had a SD of 0.73 whereas passive ones had 0.07 in an index context (“Nifty Midcap 150 Index Funds” scenario).

- For you, this means that if you prefer steadier returns with less managerial risk and are comfortable with market-level risk, passive may be the safer route. If you can stomach more risk and believe in active management, active funds might offer opportunity — but the risk is higher.

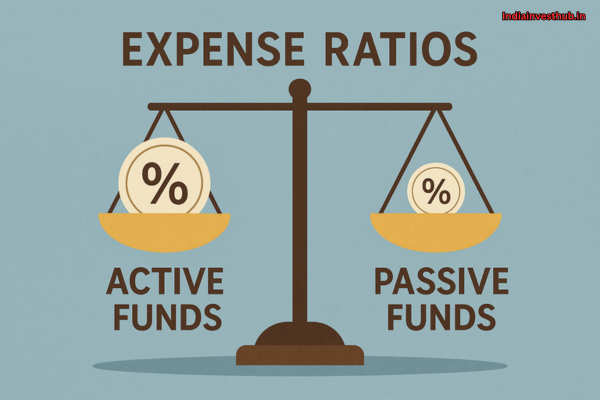

Cost Breakdown: Expense Ratios in Active vs Passive Funds

One of the most tangible differences between active vs passive mutual funds is cost — and cost eats into your returns.

- In India, active large-cap equity funds had average expense ratios of around 1.9% (or even more) compared to passive index funds which may have expense ratios in the range of 0.3% or less.

- An expense ratio might seem small-scale, but compounded over years it matters significantly. For example, one blog explains that if you invest ₹10,000 in a fund with 2.25% expense ratio, daily you effectively lose ~0.00616% from returns due to cost.

- For you, every percentage point of cost paid by you reduces your net returns. So when evaluating funds, comparing the expense ratio is a must. Especially in active funds, you want to ask: “Is the higher cost justified by higher returns (after cost)?”

Returns Analysis: Historical Performance of Active vs Passive Funds in India

When you ask “which strategy maximizes returns?”, the historical performance data is one of your main guides (though past performance is not guarantee of future results).

- One Indian research paper compared active vs passive funds across several benchmarks: for the Nifty 50 benchmark, passive funds averaged returns of ~11.89% vs active funds ~10.83% (a difference of about 1.06%).

- For the Nifty Midcap 150 benchmark, passive funds returned ~22.45% vs active ~21.31% (difference ~1.14%).

- For other benchmarks (small-cap etc) there were cases where active funds outperformed passive — e.g., for Nifty Smallcap 250, active funds returned ~27.04% vs passive ~21.70% (difference ~5.34%) in that study.

- From the global angle, a study showed that over the 10-year period ending 2024 in the US, less than 22% of active large-cap funds survived to beat indexed peers.

What does this mean for you?

- In large-cap efficient markets in India, passive funds have on average shown a slight edge (or at least less drag) than active funds once cost and risk are accounted for.

- In less efficient segments (mid-cap, small-cap) active funds may hold potential for higher returns — but with correspondingly higher risk.

- As an investor, if your strategy is long-term wealth creation with moderate risk, passive may offer a more reliable path. If you are willing to take higher risk and do your homework, active funds in specific segments may offer upside.

Suitability: Which Investors Should Choose Active Funds and Why?

If you are the kind of investor who:

- Believes that a skilled fund manager can identify opportunities ahead of the market,

- Has a longer investment horizon and appetite for risk,

- Is willing to actively monitor or trust the fund house,

- Is comfortable paying higher fees in hopes of higher returns,

Then active funds may fit you. Particularly in segments like mid-cap or small-cap where market inefficiencies exist and a good manager may exploit them. The research from India (above) supports this nuanced view: active outperformance is more likely in less efficient segments. However, you must accept that the probability of consistent outperformance is lower, and higher cost + higher risk are real tradeoffs.

Suitability: Who Should Prefer Passive Funds for Wealth Creation?

If you are the investor who:

- Prefers a simpler approach and less frequent decisions,

- Wants to minimise cost and maximise transparency,

- Aims for long-term wealth creation rather than trying to “beat the market”,

- Is investing in the large-cap space where markets are relatively efficient,

then passive funds may be more suitable for you. With lower fees, fewer deviations, and historical data suggesting that many active funds struggle to beat the benchmark, passive investing gives you a solid path and fewer things to monitor. Especially if you’re investing via systematic investment plans (SIPs) and want to keep things “set and forget” to a degree.

Tax Efficiency Comparison: Active vs Passive Mutual Funds

Another practical aspect is tax efficiency: how do active vs passive compare?

- Because active funds tend to trade more frequently, they may generate more short-term capital gains (STCG) or trigger more taxable events. Passive funds have lower portfolio turnover, which can lead to fewer taxable events — better for long-term investors.

- In India, equity mutual funds held for more than 1 year qualify for Long-Term Capital Gains (LTCG) tax (in many cases) and benefits. The less you trade, the fewer taxable events, which improves your net returns.

- What this means for you: if tax matters (and it usually does), passive funds may give you an advantage because they keep the cost and turnover low.

Active vs Passive in 2025: Market Conditions and Future Growth Predictions

Looking ahead, the investment environment in 2025 presents interesting angles for active vs passive funds. Some points to consider:

- In India, passive funds are gaining traction: for example, passive fund inflows in India in September 2025 stood at ~₹19,056 crore, signalling strong interest.

- The regulatory & structural environment is increasingly transparent; large-cap markets are becoming more efficient, reducing the opportunity for active managers to consistently outperform. As one FundsIndia article noted: the odds are stacked against active large-cap funds given high expense ratios and low active share.

- But there may still be pockets of opportunity: in small-cap, mid-cap, niche sectors or themes, where market inefficiency is higher — an active manager with skill might add value.

- For you as an investor in 2025, the takeaway is: if your strategy is broad-based large-cap equities and you’re cost-sensitive, passive likely remains the prudent choice. If you’re chasing higher returns, willing to accept volatility and cost, an active strategy may still have appeal — but your fund choice becomes crucial.

Conclusion:

Active vs Passive Mutual Funds: Which Strategy Maximizes Returns? The answer is: it depends — on your goals, risk appetite, cost sensitivity, time horizon and how much effort you’re willing to put in. For many investors seeking long-term wealth creation with moderate risk and minimal fuss, passive funds provide a compelling path: lower cost, fewer moving parts, and data showing many active funds struggle to beat the benchmark after cost. But for investors ready to dig deeper, accept higher risk, and trust in a fund manager’s skill — active funds may still hold upside, especially in less efficient segments. Ultimately, the strategy you choose should align with you — your objectives, your comfort with volatility, and your horizon.

So — for you as an investor wanting to know “Active vs Passive Mutual Funds: Which Strategy Maximizes Returns?”, which camp feels like the right one to back?