Bond Prices matter more today than ever before, especially in a world where interest rate changes can shift market sentiment overnight. Many investors follow stock trends closely, but often overlook the bond market, even though the global bond market is over $133 trillion, larger than the global stock market by a significant margin (Source: Securities Industry and Financial Markets Association, SIFMA).

When interest rates move, bond prices respond quickly, and understanding this relationship is one of the most helpful skills an investor can develop. Investors don’t need complicated math or financial jargon—just a clear explanation of how interest rates shape bond values and how this knowledge can guide smarter investment decisions.

What Are Bond Prices?

Bond prices represent the current market value of a bond. When you buy a bond, you lend money to a government or company, and in return, you receive interest (called coupon payments) and your principal at maturity. In liquid markets, bond prices fluctuate daily based on demand, market conditions, and interest rate changes. According to the Federal Reserve, the average daily trading volume in U.S. Treasuries exceeds $600 billion, indicating that bond prices adjust constantly as investors interpret economic signals.

Bonds Explained: A Complete Beginner’s Guide to Fixed Income Investments

For beginners, the key idea is simple: bond prices change because investor expectations change. When the economy strengthens, interest rates may rise. When it slows, interest rates may fall. These broad shifts affect every type of bond on the market.

How Interest Rates Work: The Foundation of Bond Pricing

Interest rates—usually set or influenced by central banks—represent the cost of borrowing money. When a central bank increases interest rates, loans become more expensive; when it lowers rates, borrowing becomes cheaper. The U.S. Federal Reserve, for example, raised rates 11 times between 2022 and 2023, the fastest tightening cycle in decades (Source: Federal Reserve Monetary Policy Reports). Each rate hike immediately created ripples across the bond market.

For investors, understanding interest rates is essential because they set the benchmark for how attractive existing bonds are. New bonds issued at higher interest rates look better to investors, causing older bonds with lower coupon rates to decline in price.

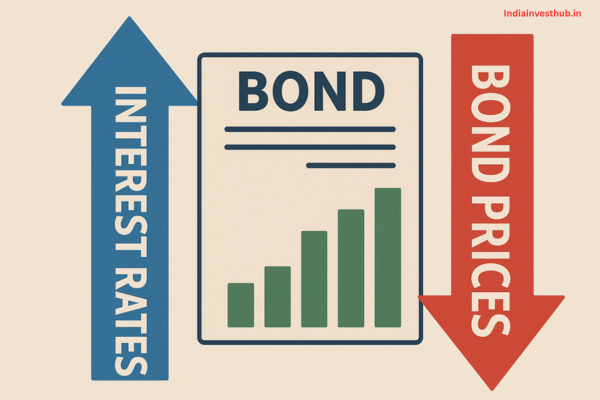

The Inverse Relationship: Why Bond Prices Fall When Interest Rates Rise

The most fundamental rule of fixed-income investing is the inverse relationship between interest rates and bond prices. When rates go up, bond prices go down. When rates fall, bond prices go up.

A simple example:

If you hold a bond paying 5% interest and new bonds start offering 7%, your bond loses appeal. Investors prefer the new ones, so your bond’s price must drop to compensate. This isn’t theoretical—during the 2022 rate hikes, the Bloomberg U.S. Aggregate Bond Index fell by 13%, its worst annual decline in history (Source: Bloomberg Markets). The steep fall wasn’t due to credit defaults but purely because rising rates pushed down bond values.

Coupon Rate vs Market Rate: How They Determine Bond Value

The coupon rate is the interest rate printed on the bond. The market rate is the currently prevailing interest rate in the economy. When the coupon rate is lower than the market rate, the bond trades at a discount (below face value). When the coupon rate is higher than the market rate, the bond trades at a premium (above face value).

For example:

- A 4% coupon bond in a 6% market trades at a discount.

- A 7% coupon bond in a 5% market trades at a premium.

This adjustment ensures all bonds offer competitive returns, regardless of when they were issued.

Yield to Maturity (YTM): What It Means and Why Investors Should Care

Yield to Maturity (YTM) tells investors the total return they will receive if they hold the bond until maturity. It includes coupon payments, price changes, and time to maturity.

Investors track YTM because it reflects the true earning potential of a bond. When interest rates rise, YTM rises too because bond prices fall. In 2023, the average YTM on U.S. Treasury bonds climbed above 4%, the highest in over a decade (Source: U.S. Department of the Treasury). For investors, rising YTM signals improving returns—if they’re willing to tolerate temporary price drops.

Duration and Convexity: Key Metrics Influencing Bond Price Sensitivity

Duration measures how sensitive a bond is to interest rate changes. Longer-duration bonds react more sharply to rate movements. Convexity measures how the price-yield relationship curves as interest rates shift.

Key points:

- Long-term bonds fall more in price during rate hikes.

- Short-term bonds are less sensitive and more stable.

- High-duration portfolios suffer most when interest rates rise.

During the 2022 rate hike cycle, long-duration bond ETFs lost 20–30%, while short-duration funds saw much smaller declines (Source: Morningstar).

Short-Term vs Long-Term Bonds: Which Are More Sensitive to Rate Changes?

Short-term bonds (1–3 years) feel minimal impact when rates rise.

Long-term bonds (10–30 years) face large price swings.

For example:

- A 30-year Treasury bond fell nearly 33% in 2022.

- A 2-year Treasury note fell only about 4%.

(Source: U.S. Treasury Historical Data)

This difference matters because investors often assume all bonds are equally “safe.” While the issuer may be safe, the price stability depends heavily on maturity.

Impact of Central Bank Policies on Bond Markets:

Central banks influence interest rates through:

- Rate hikes or cuts

- Bond-buying programs

- Inflation control policies

- Forward guidance (communication about future rates)

During the COVID-19 crisis, global central banks bought trillions in bonds, pushing yields to historic lows. When inflation surged, tightening policies reversed the trend. According to the International Monetary Fund (IMF), more than 70% of global central banks raised rates in 2022, directly impacting global bond markets.

How Rising Interest Rates Affect Corporate vs Government Bonds:

Government bonds, like U.S. Treasuries or Indian G-Secs, generally react to rate changes based on duration and demand. They are considered safer because governments are less likely to default.

Corporate bonds respond to:

- Interest rate movements

- Company financial health

- Market sentiment

- Credit spread changes

During rising rate cycles:

- Government bonds fall due to rate sensitivity.

- Corporate bonds may fall more because investors demand higher yields to compensate for added credit risk.

For example, in 2022:

- U.S. Treasuries dropped ~12%.

- Investment-grade corporate bonds dropped ~15%.

- High-yield bonds dropped ~11%.

(Source: Bloomberg Index Data)

Smart Investor Strategies During High- and Low-Interest-Rate Cycles:

Investors can use several strategies:

During High-Interest-Rate Periods

- Favor short-duration bonds for stability.

- Buy bonds at attractive yields before rates peak.

- Ladder investments to spread risk across maturities.

- Consider high-quality government bonds for safety.

During Low-Interest-Rate Periods

- Lock in long-term yields before rates fall.

- Consider bond funds for diversification.

- Explore corporate bonds for higher income.

- Monitor inflation because low-rate environments often lead to rising prices.

Professional investors routinely adjust their bond strategies according to rate expectations. The goal isn’t to predict rates perfectly, but to stay prepared.

FAQs – Interest Rates Affect Bond Prices

Q1: Why do rising interest rates lower bond prices?

👉Because new bonds become more attractive, reducing demand for older, lower-yield bonds.

Q2: Is it risky to buy bonds when interest rates are high?

👉High rates can be good for new buyers—yields are higher, and long-term gains may occur when rates eventually fall.

Q3: Which bonds are least affected by rate changes?

👉Short-term government bonds typically have the lowest rate sensitivity.

Q4: Are bond funds affected the same way as individual bonds?

👉Yes, but funds don’t mature, so price declines can persist longer.

Q5: Do interest rate changes affect all countries the same way?

👉No. Each central bank sets its own policies, though global trends often influence one another.

Conclusion:

Bond Prices move for one central reason: interest rate changes. When investors understand how the bond market reacts to rate hikes and cuts, they gain a major advantage in building stable, predictable, and risk-aware portfolios. By focusing on duration, yield, central bank trends, and the difference between short- and long-term bonds, investors can confidently adjust their strategies in any interest-rate environment.

With rate cycles becoming more frequent worldwide, is this the right time for investors to rethink how they manage bond prices?